A Strategic SWOT Analysis of the Dedicated Private Cloud Services Market

A thorough strategic analysis of the private cloud services market reveals an industry with unique and defensible strengths, but one that must continuously innovate to fend off competition from the public cloud and address its own inherent complexities. The market's most significant and enduring strength is the superior level of security, control, and data privacy it offers. A formal Private Cloud Services Market Analysis consistently demonstrates that the single-tenant, dedicated nature of a private cloud is its core value proposition. This isolation eliminates the "noisy neighbor" performance risks of a shared environment and provides organizations with granular control over their security posture and data placement. This is not just a preference but a strict requirement for many organizations in regulated industries like finance, healthcare, and government, who must adhere to stringent data sovereignty and compliance mandates. This ability to provide a cloud-like experience within a controlled, auditable, and physically or logically isolated environment is a powerful strength that the public cloud, by its very nature, cannot fully replicate, ensuring a persistent and valuable market niche.

Despite these compelling strengths, the private cloud model is beset by several significant weaknesses. The most prominent of these is the higher total cost of ownership (TCO) and the significant upfront capital expenditure required for on-premises deployments. Unlike the public cloud's pay-as-you-go model, building a private cloud requires a major investment in hardware, software licenses, and data center facilities. Even with a hosted private cloud model, the cost is generally higher than comparable public cloud services due to the dedicated infrastructure. Another major weakness is the complexity of management. Building and operating a true private cloud requires a highly skilled IT team with expertise in virtualization, networking, storage, and automation. This skills gap can be a major barrier to adoption for many organizations. Furthermore, the pace of innovation in private clouds tends to lag behind that of the public cloud hyperscalers, who are constantly rolling out new services and features at a speed that is difficult for on-premises software vendors to match.

The opportunities for the private cloud market are intrinsically linked to the broader trends of hybrid IT and edge computing. The most significant opportunity lies in positioning the private cloud as the essential core of a hybrid cloud strategy. Very few enterprises are "all-in" on the public cloud; most operate a mix of workloads across on-premises data centers and multiple public clouds. The opportunity for private cloud vendors is to provide the management and orchestration platforms that can create a seamless, unified control plane across this hybrid estate. This allows organizations to manage their applications and infrastructure with a consistent set of tools and policies, regardless of where they are physically located. Another massive opportunity is in edge computing. As the Internet of Things (IoT) and real-time applications proliferate, there is a growing need to deploy small-scale, private cloud infrastructure at edge locations like factory floors, retail stores, or cell towers. This allows for low-latency data processing close to the source, and the private cloud model is ideal for providing the necessary control and security in these distributed environments.

Conversely, the market faces a primary and existential threat from the relentless innovation and expansion of the public cloud providers. The major hyperscalers (AWS, Azure, GCP) are continuously improving their security, compliance, and governance features, slowly eroding the unique selling points of the private cloud. They are achieving more certifications and offering more tools for data residency and control, making the public cloud a viable option for an ever-wider range of regulated workloads. Another threat comes from the rise of Software-as-a-Service (SaaS). As more business functions move to fully managed SaaS applications (like Salesforce for CRM or Workday for HR), the underlying infrastructure becomes irrelevant to the end user, reducing the overall demand for IaaS and PaaS, whether public or private. Finally, the aforementioned skills gap is a threat in itself; if organizations cannot find or afford the talent to run a private cloud effectively, they may be forced to choose the simpler, managed public cloud alternative, even if it is not their ideal choice from a control or security perspective.

Discover Localized Data And Forecasts Across Key Global Regions And Individual Country Markets:

Apac Private Cloud Services Market

Argentina Private Cloud Services Market

Brazil Private Cloud Services Market

Canada Private Cloud Services Market

China Private Cloud Services Market

France Private Cloud Services Market

Categorias

Leia mais

Skin tags and warts are common skin growths that can appear on different parts of the body, causing discomfort, irritation, or cosmetic concern. According to the best dermatologist in Riyadh, understanding when these growths are harmless and when professional evaluation is necessary is essential. Early consultation helps ensure proper treatment, prevent complications, and maintain healthy...

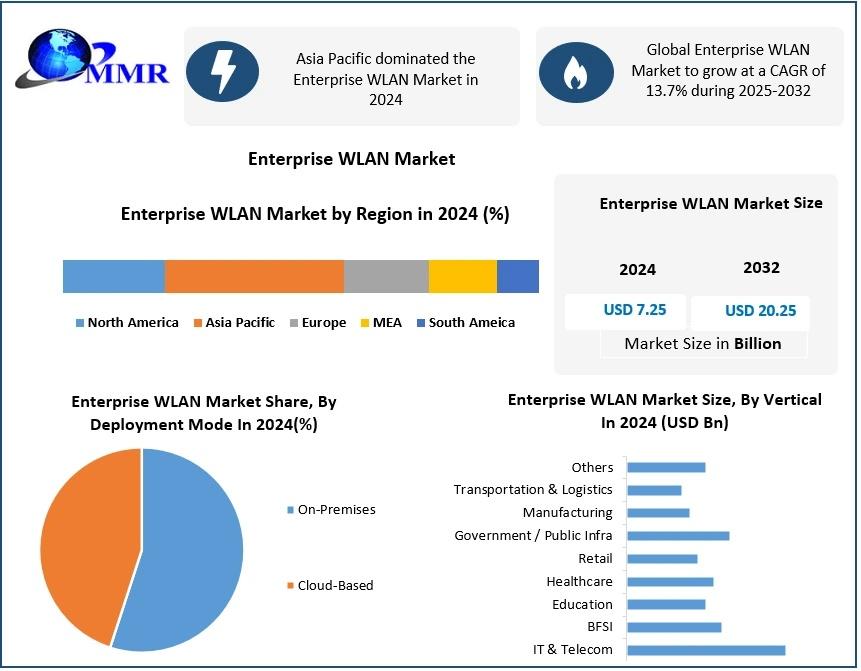

Anticipated Growth in Revenue: The Enterprise WLAN Market was valued at USD 7.25 billion in 2024, and total global Enterprise WLAN Market revenue is expected to grow at a CAGR of 13.7% from 2025 to 2032, reaching nearly USD 20.25 billion. Growing demand for high-speed wireless connectivity across enterprises. Enterprise WLAN Market Overview The report focuses on key players in the...

The Tactical UAV Market is increasingly recognized as a cornerstone of intelligence-led warfare. Tactical UAVs provide real-time battlefield visibility, enabling armed forces to conduct precision operations with minimal collateral damage. The Tactical UAV Market is projected to grow from USD 6.93 billion in 2025 to USD 12 billion by 2035, with an expected compound annual growth rate (CAGR)...

Introduction The global Fucoxanthin Market is gaining strong momentum as industries across food, pharmaceuticals, nutraceuticals, and cosmetics increasingly shift toward natural, bioactive ingredients with proven health benefits. Fucoxanthin, a marine-derived xanthophyll carotenoid primarily obtained from brown seaweeds and microalgae such as Phaeodactylum tricornutum, has...

As per Market Research Future analysis, the Autonomous Farm Equipment Market Size was estimated at 33.2 USD Billion in 2024. The market is projected to expand from 40.28 USD Billion in 2025 to 278.74 USD Billion by 2035, reflecting a compound annual growth rate (CAGR) of 21.34% during the forecast period 2025 - 2035. Autonomous technologies are redefining agricultural operations, enhancing...